A six-figure writer on the top financial mistakes you’re making as a freelancer and how to fix them, fast.

Somewhere around the middle of last year, I got a panicked email from my accountant in India. He’d just finished doing my taxes—several months late because of my tardiness—and had realized that my tax bill was going to be, let’s just say, “humongous.”

Considering that I’d left the country by then and my receipts were in a box somewhere at my parents’ house in Delhi, there wasn’t much he could do to reduce said bill.

He was not pleased about this. Considering that this would set me back financially in more ways than one, I was not pleased about this. “Stupid tax,” I said to my husband over dinner one night. “I’m not just paying tax, I’m paying for having been so stupid as to not have done this properly or on time.”

That incident taught me an important lesson.

Over the last few years, I’ve been directing my entire focus on earning more and better. I’ve done so, successfully, while working half the hours.

However, increasing income is only one part of the equation. Managing it when it comes in is the other part. And that’s sometimes the hardest part for freelancers because the money that comes in often comes in fits and spurts and is so unpredictable that it can be hard to stick to a budget or make any kind of true estimation as to what to put away into retirement funds.

You’re learning everything you can on how to make money as a freelancer.

But are you also learning how to hold on to it?

If you’re like most of the creatively gifted, mathematically challenged freelancers I come into contact with each day, the answer is probably “no.”

Most freelance writers, it might not shock you to discover, don’t have separate business accounts, projected income statements, or even a grasp on their basic cash flow for the month.

This not only keeps them feeling like they’re constantly struggling even when they’re not, but also robs them of opportunities to grow and expand their freelancing business.

Here’s a list of the top financial mistakes you could be making as a freelancer and how to fix them, fast.

FINANCIAL MISTAKES IN MINDSET

1. Having a poverty mindset

There is far too much poverty thinking in the freelancing community. It sounds like this:

- “I live in a developing country, so I can’t make as much money as freelancers in the West.”

- Freelancing is a beggar’s market.”

- “The market is shrinking and there are no opportunities.”

- “There’s just no respect for freelancers.”

- “The average pay rates are so low, how can a freelancer survive?”

- “Sometimes it feels like a job at McDonald’s would be more profitable.”

- “It’s so hard making money as a freelancer.”

Recognize any of these limiting beliefs?

A few months ago, a woman wrote to me saying she’d been offered regular freelancing work, but that it was at a much lower rate than she would have liked. Her question was whether to accept the low rate given her family circumstances, but it’s a sentence towards the end of her email that caught my attention. “I know I should be grateful that they’re paying me at all. But I feel like I want more.”

I don’t need to lay out what’s problematic about this attitude. You know. We all do. We all do it in different ways.

What I’m saying is, we must stop.

The first step to financial success is believing that it can be done. If you’re not convinced you can make six-figures, no strategy in the world can get you there.

(Here’s a practice that can help you get rid of limiting beliefs.)

If you want to succeed as a freelancer, the most important gift you can give yourself is to believe that you can.

2. Not having a profit motive

If I had to sum up my belief system about the arts in one sentence, it would be this: Art and business must co-exist.

When you create, be an artist. Don’t allow the world to tell you what your art should be or how you should create it.

But when you’re done with the art, take off that artist cap, and become a businessperson. Sell the shit out of that thing.

That’s what I believe. I believe that when I’m in my office working, I’m shut off from the world and no one can dictate to me what I can or cannot create. But when I’m done, I’m all business. I pitched the best, most kickass agents I could find for my novel, I price my courses in a way that only brings me serious students who will take action, and I will frequently ask for double of what I’m offered for freelancing assignments and walk away with it.

I have a profit motive. I not only intend, but expect to make money with my art. And so I do.

3. Not investing in your education

There are actions you can take that will increase your income. Not today, not tomorrow, not even next month perhaps, but in the long run, investing in your education through books, courses, and conferences grows your potential and your skills, which increases your income. Simple, right?

So why do people resist spending money on their education?

As someone who runs a number of trainings and online courses, I don’t need to tell you I’m a massive fan. I believe in education so much, in fact, I want to create a whole massive university for writers—come, get what you need, and go change your life and your career with it. (2023 update: I did! Check it out here.)

I invest in learning about new subjects and skills constantly, even though, yes, it always feels like a bit of a risk when I’m shelling out money for a course. It pays off, though. It always pays off.

Productivity coach Brian Tracy has a rule he lives by: 10% of his paycheck is donated, 10% is given to himself, his future, that is, he saves or invests it, and 10% is invested in his education. By his recommendation, if you earned $30,000 last year, you should have spent $3,000 of that on your education. Did you?

How about $1,500? How about $300?

FINANCIAL MISTAKES IN BUSINESS SETUP

4. Mixing personal and business finances

In a survey conducted by CreditDonkey.com, only 22.3 percent of freelancers said they had a credit or debit card dedicated solely to business expenses. In fact, most were mingling personal and business finances, a surefire way to taxation disaster, if nothing else.

But mixing your business and personal finances has other, bigger consequences as well. If you don’t know how much you’re bringing in with your freelancing and not tracking expenses, you don’t know your gross and net income numbers for the year. This means you don’t know if your income is rising or falling yearly and also whether you really are making the money that you need to be. This affects all areas of your life. If you took on a job, you’d want to know how much you’re making and budget your lifestyle accordingly, right? Same deal with freelancing.

Unfortunately, most freelancers routinely overestimate their earnings and underestimate their expenses, and this then leads to debt, stress, and crisis.

5. Not putting away money for tax

Learn from me, people. Do not get hit with a huge tax bill in the middle of the year because of your stupidity and end up paying more than you should have to. In India, I could afford to be lax and flexible because even at a high rate of income tax, the hit wasn’t so bad I couldn’t handle it. When we moved to the UK, however, I realized I’d be paying anywhere between 20-45% of my net income for the year and there was no way I’d be able to come up with that quickly. So, starting with the very first paycheck of the year, I diligently put aside 20% into a separate dedicated bank account. When the bill comes due, I’ll be able to pay it.

(Warning: Do not dip into this when sudden expenses pop up or use it as an emergency fund. Don’t ask me how I know.)

6. Not creating a foundation for your financial future

Speaking of emergency funds, having no reserve when cash flow gets tight (which it will) can shatter your business and send you back into full-time employment like nothing else can or will.

Before you do anything else, be smart and put together a financial reserve for when clients stall on payments, you get sick and your marketing has suffered, when the car breaks down, or a number of different crises that result in a need for extra cash. The emergency fund keeps you from using a credit card or pulling from your retirement savings. I suggest that freelance writers have a large emergency fund of between six and twelve months of living expenses so that you can survive a partner’s job loss, your own changing career goals (time off for a novel, for instance), and other emergencies.

When you have a financial cushion, you have freedom. It’s not sexy, but doing this will allow those more glamorous things to follow.

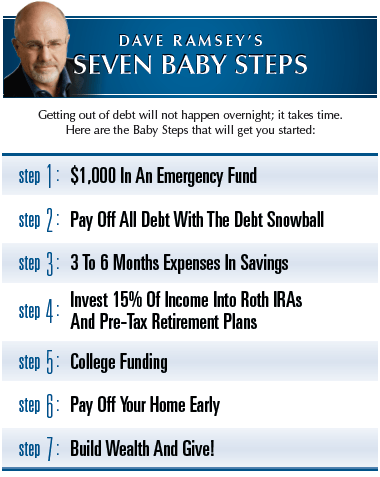

If, like me, you like to follow plans, financial guru Dave Ramsey has a popular seven-step system.

7. Not writing off all expenses

I’m so crap at this, like you wouldn’t believe. I don’t save receipts for coffee and travel, I forget to use the debit card from my business account and put it on the personal one instead, and I almost never track expenses. See, it’s all habit. For years, when I was setting up my career in India, I had no need to do all this. A coffee, a hard drive, who cares? I was in a low tax bracket and so didn’t worry about expenses, and that habit stuck. Now I’m trying to change it, and it’s harder.

For years, I excused my ineptitude by putting it under the veil of “I’m a creative type.” Now I call it exactly what it is: Stupid.

FINANCIAL MISTAKES IN DAY-TO-DAY BUSINESS

8. Failing to send or follow up on invoices

Everyone hates invoicing. Well, I like it if the bank balance is looking slim and I feel like I’ve done something productive, but mostly, I really hate the minutiae that goes with administrative tasks.

Here’s my secret: If I don’t want to do something, I try to do one of three things with it—outsource it, automate it, or get rid of it completely.

Since invoicing is important, I can’t get rid of it completely. So I could hire a VA to do it or I could automate it. I’ve chosen the latter option and with a subscription to Freshbooks, I’ve basically rid myself of the need to worry about creating a new invoice every time. Now, once a client is in my system on Freshbooks, I can send out an invoice in less than five minutes. I also set reminders for following up, so that if someone still hasn’t paid me, say, two weeks after receiving the invoice, they get sent reminders.

I use Freshbooks and my calendar, but you can use whatever method feels comfortable and less work for you.

9. Not diversifying

In my report Secrets of Six-Figure Freelancers (download a free copy here), I talk about how freelancers who make six figures are routinely trying new things and diversifying in terms of sources of income. Many of them have self-published ebooks, and a lot of them jumped into content marketing when it was in its early days. They got a ton of experience and made fantastic money with it (I’ve made as much as $475 an hour with my content marketing work.)

You need to diversify. Diversify with clients, diversify with streams of income, and diversify the kind of work you do. You can recover quicker from a lost client who makes up 10% of your income than one who makes up 50%.

I’ve taken diversification to an entirely new level. Not only just in the business of what I do (journalism, essays, content marketing, nonfiction books, novels, courses) and in how I do it (hourly income, passive income, royalties), but also in where I do it. I am an Indian freelancer living in London and have written for publications in over 200 countries.

10. Ignoring cash flow

In January 2014, a few unexpected life expenses hit me all at once: a huge medical bill, my son’s preschool fees, and car and health insurance that needed to be renewed. I should have been able to take care of these with no issues. I had just had an excellent month, billing more than $7,000, but there was little money in the bank for these expenses.

As I sat there desperately calculating why I was so broke and why I hadn’t been earning enough, I realized clients owed me over $9,000 for previous projects. My problem wasn’t income. It was cash flow.

That month, I created what is now a staple of my business: The Cash Flow sheet.

This simple Excel sheet allowed me to take control of my cash flow and figure out my projected incomings for the next few months. The trick was not to just list my payments once I received them, but to set up a system that took the lag between submitting the work and finally getting paid into account.

Here’s how I did it:

- On the top horizontal row, I made a list of months.

- In the left-hand column, I made a list of all my clients.

- Then, I looked over my assignments for the last few months and figured out when I was likely to be paid for them.

(If you’d like a done-for-you sheet that you can simply copy, download mine here.)

For instance, client #1, a national newspaper, had assigned a story in early January. I’d submitted it a week before I created the spreadsheet and I was typically paid by this publication two weeks after invoicing. That meant I would be paid in February. I entered the amount of that payment in the February column in front of the publication’s name. I went through my entire list in this way and after I was done, I could add up the projections for each upcoming month.

It’s May now, so look at the May, June, and July columns in your spreadsheet. Is there enough coming in over the next three months to keep your bills paid, or do you need to start pitching and getting some quick hits? Keeping a close track of your finances will help you answer these kinds of important questions quickly and accurately.

Here’s what this looks like:

FINANCIAL MISTAKES IN YOUR PERSONAL SETUP

11. You continue to pile on debt

Debt is death to a freelancer. I remained allergic to debt for my entire freelancer career, then last year, took on a massive amount of debt due to a cross-continent move. (India to the UK is expensive!) We should have waited to cash flow it, but there was a six-figure job on the line, we thought it would last, blah blah blah—you’ve all been there, right?

Here’s what I learned: Nothing makes you more desperate and less creative than money problems.

Remember what I said about not letting anyone or anything influence your art while you’re creating it? Well, you can’t do that if you can’t take risks. And you can’t take risks if you have debt and lack an emergency fund. When you’re worried about money, the creativity just flies right out of you and all you can think about is whether this project will pay the bills.

I think you should sell your art for craploads of money. I certainly do and intend to. But you should never create it for the money.

And that becomes near impossible when you continue to borrow money to fund your lifestyle.

12. Not having insurance

Do I need to say anything? We all know it. Most of us don’t do it.

Granted, with all the moving around international freelancers do, it’s very difficult to get good insurance, stick to it, and make it work. But I think that because we move around so much, it’s even more essential.

I don’t need to sell you on this. Seriously, just put aside some money and do it.

13. Not accounting for sick days

When I used to do my yearly projections, I counted 365 days of work. Then, after I had a child and realized I liked having the weekends and bank holidays off to spend time with my son, I cut that back down to 200 days.

But that still doesn’t account for sick days (mine and my son’s). It doesn’t account for holidays.

I get sick during the year and take days off. I take holidays during the year and take days off. Then I wonder, at the end of the year, why my projections were so off. Duh.

Account for sick days.

14. Waiting for Prince Charming

This is a phrase I’ve taken from rockstar financial guru and kickass author Barbara Stanny, who I consider one of my financial mentors and go-to people for financial advice. Barbara has a book called Prince Charming Isn’t Coming: How Women Get Smart About Money and in it, she talks about how people, especially women, keep waiting for things to materialize and “save” them from their financial predicament. This could be men, sure, hence the title of the book, but for self-sufficient women like me, it could be other things.

I did, for quite a while, wait for a book deal to solve all my financial problems. A six-figure book deal had been on the horizon and I expected it would make up for all the not-so-smart money decisions I made while waiting for it. It didn’t come, and I learned the very important lesson that you can’t wait for Prince Charming—what we call “big wins” in our household—to get you out of trouble.

The big wins may or may not come. I sure hope they do. I’m working towards making it so that they do. But in the meantime, I’ve got to do the everyday work anyway. I’ve got to keep getting those small wins because they add up, too.

FINANCIAL MISTAKES IN PRICING AND NEGOTIATION

15. Thinking a client’s offer is the final offer

If you’ve been around this website or me for any length of time, you know that I’m big on negotiating. For me, not negotiating is akin to not trying. When you fail to negotiate, you’re basically saying, I’m too scared/lazy/fill-in-the-blank to write one extra sentence that might increase my income on this project by a substantial amount.

I’m not coy about negotiating. I’ve written before about how when editors email me with a rate, I’ll ask for double that. Often, I’m surprised how quickly they’ll just agree to it. Just like that. Because I asked.

Don’t leave money on the table. If you’ve read up to here, you’re serious about changing your finances. So roll up your sleeves and learn how to negotiate.

16. Not charging a rush fee

You know when a client emails you on a Friday afternoon, wanting work on a Monday, and you want the work and the money and just say yes? I did exactly that last weekend. I was off to Legoland with my son and I was packing and sorting things out, trying to get through them quickly and feeling extremely distracted. In the middle of all that, an email arrived from a client asking for a rush job and instead of saying, well, that will cost extra because I need to be paid for writing this fast, I completely flaked and said yes.

Learn from me, people. (Are you sensing a theme of “I’ve made a shit ton of mistakes, so don’t be me” here?)

I have suffered, so you don’t have to. Ask for a rush fee—anywhere from 25 to 50% extra—for any work that needs you to be available over the weekend or for which you’d need to rearrange your life.

17. Not calculating your hourly rate

Let me be clear: You don’t have to charge an hourly rate (in fact, you probably shouldn’t). But you must know your hourly rate.

Not calculating an hourly rate is especially true for magazine writers and journalists. They don’t see the point. But I know, from experience, that when I was writing exclusively for magazines and newspapers, the only way I could grow my income was to track how much time I was spending on each piece and then calculating the per hour rate on individual projects. This allowed me to see that the $1-a-word magazine feature, which seemed high-paying, actually made me the least amount of money in terms of time spent. The $100 blog posts I whipped off without much thought in half an hour? They proved to be far more profitable, especially when they came in on a recurring basis.

It’s not that I let go of my feature writing completely. I didn’t and I won’t because it’s not all about the money, but it allowed me to see which work I needed to push more of when money got tight, or where I needed to direct my focus if I wanted to increase my income. It also became fun for me to try to do my work in fewer hours, eliminating some of my tendencies towards distraction and procrastination.

I also, of course, hold on to certain low-paying clients because they pay quickly and, therefore, help with my cash flow.

18. Charging too little

Just double your rates. Seriously. If you’re making less than six-figures a year with your freelancing, you’re not charging enough.

Raise your rates. Routinely, unapologetically. Let go of lower-paying clients gradually. It’s called growth.

19. Not offering enough value for what you charge

There is no such thing as pricing too high. I truly believe that. But there is such a thing as not offering enough value for what you charge.

For instance, I posted an ad a while ago saying I needed someone to manage my email and do some very basic VA work for me. I had several people quoting me $100 an hour for this work. They wanted to charge what they were worth. Fair enough.

However, while you may be worth a lot more than $100 an hour, answering email itself is not a high-value activity. You can only negotiate and demand high rates (and you should) when you provide something of value that is greater than that price.

Remember, under promise, over deliver.

If you want to increase your income, don’t just increase your rates. Increase your value.

20. Thinking “money earned” is the same as “money received”

Remember my cash flow story? This is an addendum to it.

So, you know you’ve got this assignment that will pay $2,000 and you’ve counted that as money earned. But you can’t—or shouldn’t, rather—allocate this money to future expenses until it translates to money received, which is assignment submitted, editor pleased, money in the bank.

Because, you know—and you do know—that there are several steps between money earned and money received that can lead to money not received, such as assignments getting killed and publications going out of business or editors who just can’t be bothered to pay you the $500 for the assignment you completed with a sick baby on your lap. (I’m looking at you Girls’ Life. And yes, I’m still waiting, four years later.)

If you allocate it and don’t receive it, that can set you back.

FINANCIAL MISTAKES IN TRACKING

21. Not tracking the numbers in your freelancing business

Because if you don’t know what’s coming in and going out, how are you ever going to improve it, right?

I wrote a post on the six numbers in your freelancing business that you simply can’t afford to ignore. They are:

- Number of clients

- Amount earned

- Amount billed

- Amount received

- Hourly rate per assignment

- Words written per day

We’ve talked about some of these numbers above. But if you want a complete overview of how I organize my freelancing life by the numbers, this post will give you the breakdown.

FINANCIAL MISTAKES IN PLAYING WELL WITH OTHERS

22. Not hiring an accountant

Are you a financial expert? Would you trust yourself to take over the accounts of the local grocery store down the road? No.

Well, then why the heck would you trust your own business accounts to you? If you wouldn’t trust yourself with the numbers of someone else’s business, why on earth would you do so with your own?

Please. Don’t.

Get an expert. You’re looking at the financial advisor or accountant as a cost, but trust me, by the time they’re done with your accounts, they’ll have saved you more money than what they cost. People hire you because you’re the writing expert and will catch what they’ve missed. It’s the same thing with the financial expert you hire.

23. Not outsourcing

Freelance creatives typically suffer from two main business maladies: The Superhero Syndrome (“I can do this myself”) and the Scrooge Strategy (“I can do this myself for free”). Inevitably, these two conditions will lead to burnout, loss of passion, and frustration. Worse, most of us don’t actually think there are parts of our business that we can outsource. You may be a solopreneur, but you don’t have to be an overworked one who does everything by yourself.

Here’s one way to think about it: Say you have a company with two employees—you pay one employee $100 an hour for high-value tasks that require planning and strategy, and you pay the other $50 an hour for administrative duties. Would you routinely ask the person getting $100 an hour to take over the administrative work?

That’s what you’re doing when you refuse to outsource and do the grunt work yourself.

It may seem unusual at first, but letting go of some grunt work and hiring an assistant can actually help you make more money as a freelancer.

What can you outsource? I wrote up this entire list for Contently’s The Freelancer blog.

24. Not asking others what they’re paid

I received an email from a freelancer friend the other day asking how much I’d been paid by a certain editor. They’d offered her $300 for a 1,000-word story and she liked the rate. There was potential for regular work. She was leaning towards taking it. I got paid $1 a word, I wrote back, so please, please, please, negotiate. She took my advice and asked for $1 a word. They gave it to her without question.

This is the value of networking, of asking others what they’re being paid, and of sharing what you’re being paid.

Money is often a subject creative people, freelance writers included, ignore because it seems too boring or difficult to have that conversation. But here’s the thing: Having enough money gives you the freedom to be creative and constantly struggling and worrying about where the next paycheck is coming from or how you’re going to feed your kid steals it.

In order to be creative and do the work that speaks to you, it is essential to create a financial situation that gives you flexibility and peace of mind. If you have that, your creative dreams can soar.

You should be an artist.

Being a business when you’re not creating helps you achieve that.

FREE RESOURCE:

MASTERCLASS: The $100K Blueprint for Multipassionate Writers

In this masterclass, I’m going to give you a step-by-step strategy to build multiple sources of income with your creative work in less than a year.

If you’ve been told you need to focus on one thing in order to succeed, this class will be an eye-opener. Watch it here.